All Categories

Featured

Table of Contents

Acquired annuities come with a fatality benefit, which can supply monetary safety and security for your enjoyed ones in the event of your death. If you are the beneficiary of an annuity, there are a few guidelines you will certainly need to comply with to inherit the account. You will certainly need to offer the insurance policy company with a copy of the fatality certification for the annuitant.

Third, you will need to provide the insurer with other needed documentation, such as a duplicate of the will or depend on. Fourth, depending on the kind of inherited annuity and your individual tax obligation scenario, you might need to pay tax obligations. When you inherit an annuity, you must choose a payout alternative.

With an immediate payout choice, you will begin obtaining settlements today. The repayments will be smaller sized than they would be with a deferred choice since they will certainly be based on the current worth of the annuity. With a deferred payment option, you will certainly not begin obtaining repayments later on.

When you inherit an annuity, the tax of the account will certainly depend upon the kind of annuity and the payment alternative you choose. If you acquire a conventional annuity, the settlements you receive will be strained as regular income. If you inherit a Roth annuity, the repayments you receive will not be strained.

Annuity Fees inheritance tax rules

Nonetheless, if you pick a deferred payment alternative, you will not be strained on the development of the annuity till you start taking withdrawals. Talking to a tax obligation advisor prior to inheriting an annuity is necessary to ensure you comprehend the tax effects. An inherited annuity can be a fantastic method to supply financial protection for your loved ones.

You will certainly also require to adhere to the guidelines for inheriting an annuity and select the appropriate payout alternative to fit your requirements. Finally, make sure to talk with a tax expert to guarantee you comprehend the tax obligation implications of inheriting an annuity. An inherited annuity is an annuity that is given to a recipient upon the fatality of the annuitant

To acquire an annuity, you will certainly require to offer the insurance provider with a copy of the fatality certification for the annuitant and complete a beneficiary form. You may require to pay taxes relying on the kind of inherited annuity and your individual tax circumstance. There are two main kinds of inherited annuities: conventional and Roth.

The taxation of an inherited annuity will depend on its type and the payment choice you choose. If you acquire a conventional annuity, the repayments you get will certainly be tired as average revenue. If you inherit a Roth annuity, the settlements you get will not be taxed. If you pick a prompt payout option, you will be exhausted on the annuity's development approximately the day of inheritance.

Taxation of inherited Multi-year Guaranteed Annuities

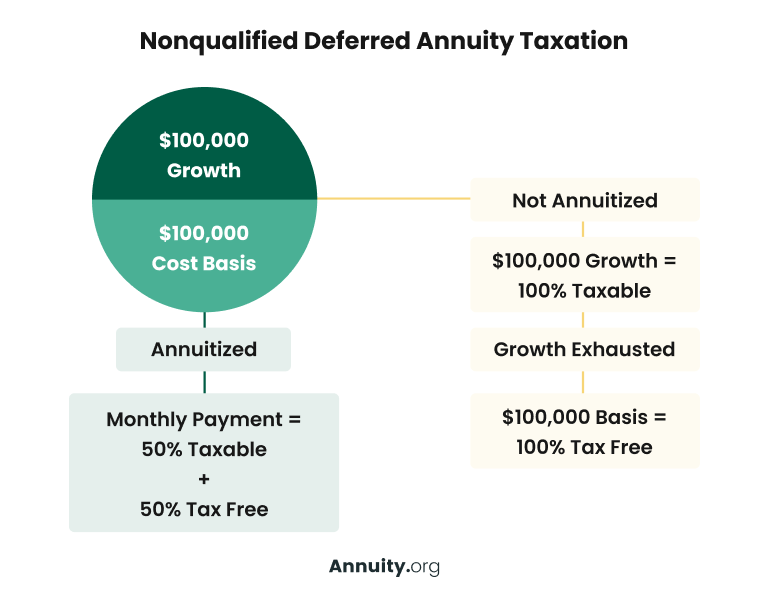

Exactly how an acquired annuity is taxed depends on a variety of variables, but one secret is whether the cash that's appearing of the annuity has actually been taxed before (unless it remains in a Roth account). If the money distributed from an annuity has not been strained before, it will certainly undergo tax obligation.

In enhancement to owing revenue taxes, you might be hit with the net financial investment income tax obligation of 3.8 percent on distributions of incomes, if you surpass the annual thresholds for that tax. Inherited annuities inside an IRA additionally have special distribution policies and enforce various other requirements on heirs, so it is very important to understand those policies if you do acquire an annuity in an IRA. A certified annuity is one where the owner paid no tax obligation on payments, and it may be held in a tax-advantaged account such as typical 401(k), standard 403(b) or typical IRA. Each of these accounts is moneyed with pre-tax cash, implying that taxes have not been paid on it. Since these accounts are pre-tax accounts and revenue tax has actually not been paid on any of the cash neither contributions neither earnings circulations will go through common income tax obligation.

A nonqualified annuity is one that's been bought with after-tax cash money, and distributions of any type of payment are exempt to income tax since tax obligation has currently been paid on contributions. Nonqualified annuities consist of 2 major types, with the tax treatment depending upon the kind: This sort of annuity is acquired with after-tax money in a regular account.

Any type of typical distribution from these accounts is cost-free of tax on both contributed money and earnings. At the end of the year the annuity firm will certainly submit a Type 1099-R that shows precisely how much, if any type of, of that tax obligation year's distribution is taxable.

Beyond revenue taxes, an heir may likewise require to calculate estate and inheritance taxes. Whether an annuity undergoes income taxes is an entirely separate matter from whether the estate owes inheritance tax on its worth or whether the successor owes inheritance tax obligation on an annuity. Inheritance tax is a tax obligation evaluated on the estate itself.

The prices are modern and range from 18 percent to 40 percent. Specific states might also impose an inheritance tax on money distributed from an estate. On the other hand, estate tax are taxes on an individual that gets an inheritance. They're not analyzed on the estate itself yet on the successor when the properties are received.

Inherited Flexible Premium Annuities taxation rules

government does not examine estate tax, though 6 states do. Fees variety as high as 18 percent, though whether the inheritance is taxed depends on its dimension and your partnership to the provider. So those acquiring big annuities ought to pay focus to whether they go through estate taxes and inheritance tax obligations, beyond just the basic revenue tax obligations.

Heirs need to take note of prospective inheritance and estate tax obligations, also.

Right here's what you need to understand. An annuity is a financial item offered by insurance firms. It's a contract where the annuitant pays a round figure or a series of costs in exchange for a guaranteed earnings stream in the future. What happens to an annuity after the owner dies rests on the specific details described in the contract.

Other annuities supply a death advantage. The payment can take the kind of either the entire continuing to be balance in the annuity or a guaranteed minimum amount, generally whichever is higher.

It will clearly determine the recipient and possibly outline the offered payment alternatives for the death benefit. An annuity's death benefit ensures a payment to an assigned recipient after the proprietor passes away.

{kind=link}

Table of Contents

Latest Posts

Understanding Financial Strategies Everything You Need to Know About Financial Strategies Breaking Down the Basics of Investment Plans Benefits of Variable Vs Fixed Annuities Why What Is Variable Annu

Understanding Fixed Annuity Or Variable Annuity A Comprehensive Guide to Investment Choices Breaking Down the Basics of Investment Plans Pros and Cons of Various Financial Options Why Variable Vs Fixe

Exploring the Basics of Retirement Options A Comprehensive Guide to Investment Choices What Is Retirement Income Fixed Vs Variable Annuity? Advantages and Disadvantages of Different Retirement Plans W

More

Latest Posts